Searched for Medline stock and couldn’t find a ticker symbol? You’re not alone. Good news — you’re about to avoid a real mistake before it costs you.

For years, Medline Industries stayed in private equity hands. Retail investors had no way in.

2026 changes that.

Want to know where Medline stands today? Curious how its IPO journey played out? Wondering if this medical supply giant belongs in your portfolio? You’ll get straight answers here.

No fluff. No runaround. Just a clear breakdown of what’s real, what’s rumor, and what smart investors are doing right now.

Yes, You Can Buy Medline Stock in 2026 — Here’s What Changed

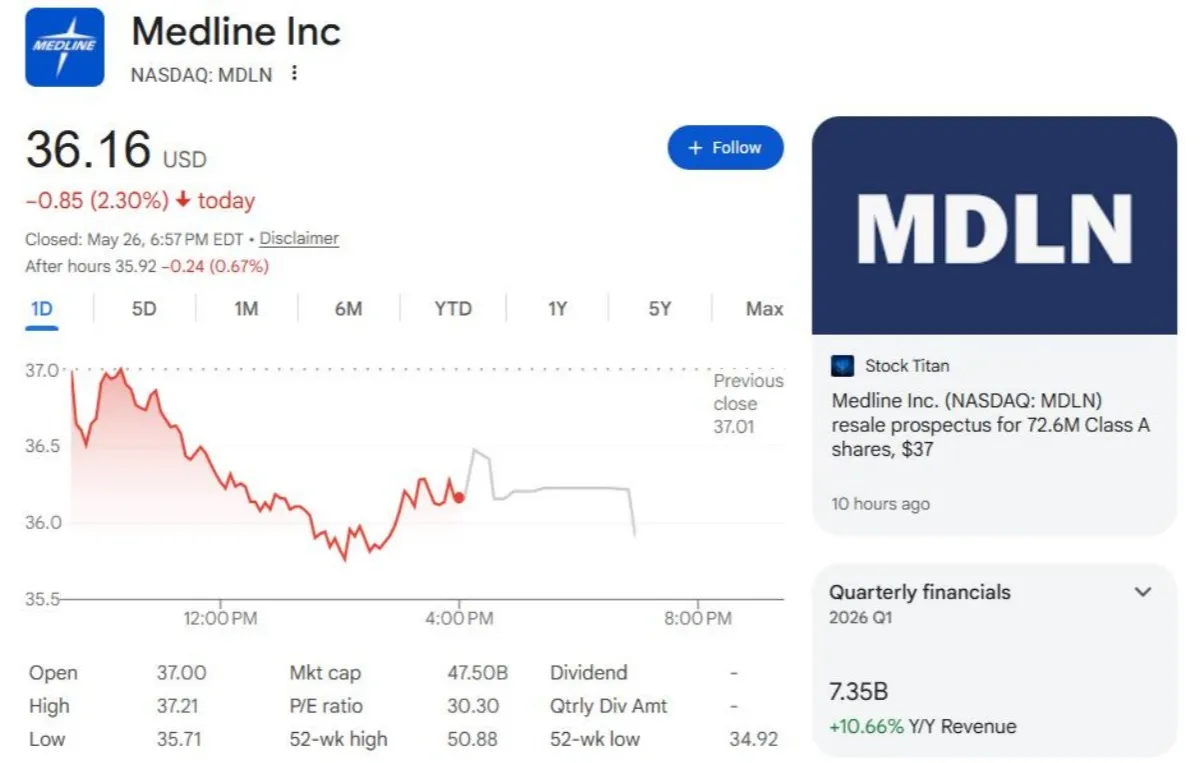

The ticker is MDLN. It trades on Nasdaq. You can buy it today through any standard U.S. brokerage account.

That’s the short answer. Here’s the full picture.

The March 2026 Secondary Offering Changed Everything

On March 10, 2026, Medline closed a massive secondary offering. 86.25 million Class A shares hit the public market at $41.00 per share. Every share came from existing private equity sellers: Blackstone, Carlyle, Hellman & Friedman, and a subsidiary of the Abu Dhabi Investment Authority (ADIA).

Medline itself sold nothing and kept zero proceeds. But that’s not the point. The real story is what this did to liquidity. Eighty-six million shares entering the public float means tighter spreads, larger tradable blocks, and genuine access for individual investors.

The private equity overhang that kept retail investors locked out? A big chunk of it just cleared at $41.

What do the Numbers Look Like Right Now?

Here’s what the data shows for investors doing real due diligence:

|

Reference Point |

Price |

|---|---|

|

Current spot price |

$36.16 |

|

March 2026 offering price |

$41.00 |

|

Analyst consensus target (12-month) |

$50.85 |

|

Analyst high target |

$62.00 |

|

3-month projected range (90% probability) |

$31.58 – $40.79 |

At $36.16, MDLN trades below the price Blackstone and Carlyle just took as their exit. That gap is worth noting.

29 Wall Street analysts now cover MDLN. The consensus? “Moderate Buy” — 21 analysts rate it a straight Buy, 2 call it a Strong Buy, and just 1 rates it a Sell. Their average 12-month target points to 40.61% upside from current levels.

Short-term, one technical model projects a −11.41% pullback over the next three months. The 90% probability trading range sits at $31.58 to $40.79. That’s not a dealbreaker — but size your position with that range in mind.

How to Buy MDLN?

-

Open your brokerage account — any platform with Nasdaq access works

-

Search ticker: MDLN — confirm the issuer shows as Medline Inc., Class A common

-

Check the live quote against the $41.00 offering price benchmark

-

Use limit orders — post-secondary spread dynamics make market orders costly. You leave money on the table with a market order.

-

Size with care — a 2–5% portfolio allocation at $36.16 works out to 138 shares per $5,000 invested

Want deeper research — earnings models, SEC filings, forward guidance? Reach Medline’s IR team at IR@medline.com or +1.847.247.7222.

Medline Stock (MDLN) Key Facts: What Every Investor Should Know in 2026

Here’s the raw data on MDLN — no noise, no narrative spin. Just the numbers that matter for your decision.

The Basics First

MDLN trades on Nasdaq under the name Medline Inc. It’s a large-cap medical-surgical products and supply chain company based in Northfield, Illinois. The company has 1.3 billion shares outstanding and a market cap of $31.3 billion. This is no speculative micro-cap. It’s an institutional-grade name in the Medical Instruments & Supplies sector.

Where Does the Medline Stock Sit Right Now?

As of late May 2026, MDLN closed at $37.01. That’s a −9.7% total return over the past 12 months. The stock moves with little drama. Daily swings under 1% are typical for a company this size. Large-cap healthcare stocks don’t often make big intraday headlines. The trend is what matters here — and right now, the trend is down.

Q1 2026 Earnings: Beat, But Close

Results released May 6, 2026, showed a modest positive outcome:

-

Revenue: $7.352 billion — beat consensus by $46 million (+0.63%)

-

EPS: $0.33 — beat consensus of $0.30 by $0.03 (+10% surprise)

Not a blowout. But a beat is a beat. Two straight metrics came in above Street estimates. That counts for something when you’re building a thesis.

What Analysts Really Think?

This is where it gets interesting. The median 12-month price target across 23 analyst ratings sits at $50.00. That implies +35% upside from current prices.

Two strong calls stand out:

|

Analyst |

Firm |

Target |

Implied Upside |

|---|---|---|---|

|

Lisa Gill |

J.P. Morgan |

$53.00 |

+43% |

|

Patrick Donnelly |

Citigroup |

$60.00 |

+62% |

Zero sell ratings reported. That’s not a small signal.

The Ownership Story Is Split

Institutional money is moving in fast. Last quarter, 228 institutions added to MDLN positions. Just 13 trimmed. That 228-to-13 ratio shows you where the smart money is leaning.

Insiders tell a different story. Over the past six months, 24 insider sales versus 4 purchases — a 6:1 ratio skewed toward selling. Management diversifying? Taking profits post-IPO? Likely both.

Don’t overlook this split. Institutions buying while insiders sell doesn’t mean trouble on its own. But it’s a tension worth tracking as Q2 results get closer.

The Gap That Defines the Opportunity

At $37, MDLN is priced where pessimism sits. The analyst community sees $50. That $13 gap between market price and the median Street target is either a real opportunity — or a sign that analysts haven’t caught up to reality yet.

Watch three things going forward:

– EPS trend relative to the Q1 $0.33 baseline

– Revenue growth versus the ~$7.35B run rate per quarter

– Whether the −9.7% price trend turns around or keeps falling

Those three data points will show you whether the analyst targets are grounded — or just optimistic noise.

How Medline Went From Private to Public: The IPO Story Behind MDLN

Medline’s path to Nasdaq stands out as one of the most striking private-to-public stories in recent memory. You’ve got a decades-old family business, a record-breaking buyout, and one of the biggest IPOs the market has seen in years.

Here’s the full timeline.

The 2021 LBO That Set Everything in Motion

In 2021, Blackstone, Carlyle, and Hellman & Friedman pulled off a $34 billion leveraged buyout of Medline. That made it the largest LBO since the 2008 financial crisis. The Mills family had built this business over generations — and they didn’t walk away. They held onto 25% ownership, making them the single largest shareholder in the company.

That LBO stacked up a mountain of debt. The IPO was the cleanup operation.

The 2025 IPO: Numbers That Broke Records

Medline is listed on the Nasdaq Global Select Market under the ticker MDLN — and it didn’t just go public. It went public at scale.

-

Initial offer price: $29.00 per share (near the top of the $26–$30 range)

-

Shares sold: ~248 million Class A shares after upsizing and greenshoe

-

Gross proceeds: $7 billion

-

Day-one open: $35.00 — Day-one close: $41.00

-

First-day pop: 41.38% above the IPO price

-

Single-day market cap added: ~ $12 billion

CNBC called it a key test case for private equity exits in 2025. At the top end of valuation talk, analysts put a potential $55 billion market cap on the table. That’s more than $20 billion above what PE sponsors paid just four years earlier.

For context: Medline posted $25.5 billion in revenue in 2024. Net sales have grown every single year since the 1960s — at an 18% CAGR. That kind of sustained growth explains why IPO demand was strong enough to push the deal from an initial 179 million shares up to 250 million.

The Up-C Structure: Why It’s More Complex Than a Normal IPO

This isn’t a standard IPO. Medline used an Up-C (Umbrella Partnership C-Corp) structure. For investors, understanding how it works is worth your time.

Here’s how it breaks down:

-

Medline Inc. (MDLN) is a traded Delaware C-corp. Buy MDLN, and this is what you own.

-

Its core asset is a controlling equity interest in Medline Holdings, L.P. — the operating partnership that holds all assets, liabilities, and business operations.

-

Pre-IPO owners (Blackstone, Carlyle, H&F, Mills family) swapped their old partnership stakes for Common Units of Medline Holdings, L.P.

After the IPO, the ownership split looks like this:

|

Ownership Class |

Shares/Units |

Economic Interest |

|---|---|---|

|

Public investors (Class A) |

~248 million |

~31% |

|

Legacy PE & Mills family (Common Units) |

~551 million |

~69% |

|

Total |

~799 million |

100% |

One detail worth knowing: legacy owners can exchange their Common Units for public Class A shares down the road. Each converted unit retires as a matching share gets issued. So the total share count stays fixed at ~799 million. No dilution.

There’s also a Tax Receivable Agreement (TRA) baked into the structure. Medline agreed to pay pre-IPO owners 85–90% of the tax benefits from the step-up in tax basis the transaction created. Most of that tax shield goes back to the PE sponsors and the Mills family — not to public shareholders.

What the IPO Actually Solved?

The ~$7 billion raised wasn’t earmarked for new facilities or product launches. The money went straight to deleveraging — paying down the debt built up from the 2021 LBO.

Private equity got a partial monetization event. The Mills family kept control. Public investors got access to a company that had never traded on the open market before — at least not since a short window in the 1970s, before it went private again.

That’s the real story behind MDLN: four years from the largest LBO of its era to one of the largest IPOs of 2025.

Is Medline Stock Worth Buying? Analyst Views and Risk Factors

The numbers tell two different stories at once. Which one do you believe will determine whether MDLN belongs in your portfolio?

Here’s the tension: 83% of 29 Wall Street analysts rate this stock a Buy. The median price target implies 40%+ upside. Morningstar’s fair value model pegs it at $69.81. Yet the stock sits 30% below its 52-week high of $50.88. Margin compression is real. Interest coverage is a genuine concern.

Both stories are true. Neither cancels the other out.

What the Analyst Community Really Believes?

The consensus is clean — especially for a company that just went public. Across 29 analyst ratings, the breakdown looks like this:

-

83% Buy

-

17% Hold

-

0% Sell

Not a single sell rating. That’s rare at any valuation level.

Simply Wall St’s model puts fair value at $55.09. That means the stock trades 20–28% below intrinsic value, depending on which model you use. Morningstar goes further — publishing a $69.81 fair value while flagging “Very High” uncertainty around that number.

TradingKey reaches a similar conclusion from a different angle. Medline is “increasingly profitable”, holds a strong position in medical devices, and fits long-term, stability-focused investors best. It’s not a stock for those chasing fast growth.

Earnings forecasts back the optimism. EPS growth is projected at 19.89% per year. The company swung from a $25M net loss in 2022 to $234M net income in 2023. From 2022 through mid-2025, it produced $1.2 billion in free cash flow. That kind of turnaround is hard to dismiss.

The Investment Case: Why the Bulls Have a Point

Three structural advantages set Medline apart from a standard distributor:

1. Vertical integration at scale. Medline manufactures a large share of what it sells. That’s a different model from pure-play distributors like Cardinal Health or Owens & Minor. Manufacturing in-house creates pricing flexibility on the sales side — a real edge with hospital systems under budget pressure.

2. Demand that doesn’t cycle out. Medical-surgical supplies for hospitals , surgery centers, nursing homes, and post-acute facilities don’t dry up in a downturn. This isn’t discretionary spending. It’s baseline purchasing that continues no matter what the economy does.

3. AI-powered supply chain. Medline’s Mpower platform is running supply chain optimization right now. This isn’t a pitch deck feature — it’s a real lever for margin recovery. Mpower delivering even 100–150 bps of EBITDA margin improvement over two years would make the bull case much stronger.

The Risk Factors You Cannot Ignore

The bull case is real. So are these four risks.

Interest coverage is weak. Simply Wall St states directly that “interest payments are not well covered by earnings.” This isn’t a footnote detail. It’s a direct result of the 2021 leveraged buyout, which loaded up debt before IPO proceeds helped pay it down. Track interest coverage as each quarterly report comes in.

Margin compression is happening now. Q1 showed 11% revenue growth — but adjusted EBITDA margin shrank by 250 basis points. Revenue rising while margins fall is the opposite of operating leverage. Return on Sales sits at just 0.07%. There’s almost no cushion to absorb cost increases or pricing pressure.

Valuation doesn’t match the margins. A P/E of 30–53x — depending on whether you use normalized or reported metrics — is steep for a low-margin medical supply distributor. Compare that to Cardinal Health or Owens & Minor. You pay far less per dollar of earnings at those companies. The premium on MDLN is a bet on future growth execution, not current profitability.

No dividend. Zero. Every dollar of return depends on price appreciation. For income-focused investors or those with shorter time horizons, that shifts the risk-reward picture in a big way.

The Bottom Line: Who Should Buy MDLN

|

Investor Profile |

MDLN Fit |

|---|---|

|

Long-term growth investor (3–5 year horizon) |

✅ Strong case — 20% EPS growth, 40%+ analyst upside |

|

Income investor |

❌ No dividend, no yield support |

|

Risk-averse/capital preservation |

❌ High P/E, thin margins, weak interest coverage |

|

The institutional-grade healthcare sector plays |

✅ Scale, vertical integration, stable demand |

|

Speculation / short-term trade |

⚠️ Post-secondary offering volatility, −9.7% recent trend |

MDLN is not a broken company. It’s a new public company — high leverage, low margins, but growing — and it trades at a growth stock multiple. Most analysts believe the gap between the current price and fair value is real. The risk factors are just as real.

You hold through the leverage overhang. You watch margins start to recover. You accept 0% dividend while waiting for the thesis to pay off. The data support that position. Those conditions don’t fit every portfolio — and for investors who need lower valuations or a longer public track record, other names in the medical supply sector offer exactly that.

Frequently Asked Questions About Buying Medline Stock

Thousands of investors search for “Medline stock” every month with the same questions. Here are the most common ones — answered straight.

Is Medline a public company? What’s the ticker symbol?

Yes. Medline Inc. trades under the ticker MDLN on the Nasdaq. The current share price sits around $37.01, with a −8.89% YTD return and zero dividend yield. It’s a growth stock — all return comes from price appreciation.

Which brokers let me buy MDLN?

Three confirmed platforms:

-

Saxo Bank — search MDLN:xnas on SaxoInvestor or SaxoTrader, buy shares with no extra steps

-

Stash — supports fractional shares at any dollar amount, no add-on commissions

-

Any standard U.S. discount broker — search MDLN, confirm the Nasdaq listing, and place your order

Can I trade MDLN using CFDs or derivatives?

Some platforms plan to offer CFDs on Medline shares. This depends on regulatory approval, so the timeline isn’t set yet. CFDs let you go long or short without owning actual shares. You also get stop-loss and take-profit controls built in. Check with your broker to confirm access before you count on it.

Could I buy Medline stock before the IPO?

No. Before the IPO , access was limited to institutional investors through private secondary markets. Retail investors could buy in after the Nasdaq listing went live.

Does Medline offer an Employee Stock Purchase Plan?

Yes. Eligible U.S. and Mexican employees can join Medline’s ESPP. You buy company stock through payroll deductions at a discount. Contribution limits and offering periods follow internal plan rules set by the company.

Conclusion

The question that brought you here has a clear answer — and now you have it.

Is Medline stock the right move for your portfolio? It comes down to one thing: do your homework before everyone else figures it out.

Medline Industries built one of the largest medical supply operations in the world. Its public market debut opens the door for retail investors who’ve been watching from the sidelines. This changes the investment picture in a big way.

Here’s what matters most:

-

Understand the company’s private equity roots

-

Respect the risk factors

-

Never overlook the traded competitors already generating shareholder returns today

Don’t just bookmark this page — take action. Open your brokerage account. Run the numbers against McKesson or Cardinal Health. Then decide where Medline Healthcare stock fits inside your broader medical sector strategy.

The smartest investors don’t wait for perfect conditions. They get in early, stay informed, and let compounding do the work.